Numbers in the text and table may not add up to totals because of rounding. In this report, revenues are reported on a fiscal year basis. (Federal fiscal years run from October 1 to September 30 and are designated by the calendar year in which they end.) All other years referred to in this report are calendar years.

E state and gift taxes are a linked set of federal taxes that apply to transfers of wealth. In 2021, estates face a 40 percent tax rate on their value above $11.7 million, although various deductions reduce the value subject to the tax. The same threshold and tax rate apply to gift taxes.

In 2020, revenues from federal estate and gift taxes totaled $17.6 billion (equal to 0.1 percent of gross domestic product, or GDP). In recent years, changes to estate and gift tax laws have reduced the revenues raised by the taxes and the number of taxpayers who incur that liability.

In this report, the Congressional Budget Office describes estate and gift taxes, the people who pay them, the types of assets that make up taxable estates, and the model the agency uses to project estate and gift tax revenues in its baseline. Here are the report’s main findings:

To project estate and gift tax liability for a representative sample of households under current law, CBO uses information from estate tax returns, the Survey of Consumer Finances, and its own economic and demographic projections.

Estate and gift taxes are often considered together because they are subject to the same rate and share the lifetime exemption amount. However, one main difference is that the estate tax applies to transfers of the decedent’s property at death, whereas the gift tax applies to transfers made during his or her life. 1 Over the past 40 years, estate and gift taxes have been changed many times; they are scheduled to change again in 2026 under current law.

When people die, their assets become the property of their estate. Everything a decedent owned or had a financial interest in at the time of death—from stocks and buildings, for example, to jewelry and artwork—is considered part of his or her estate. If the value of the decedent’s gross estate exceeds $11.7 million in 2021, then the executor of the estate must file a federal estate tax return, even if no amount is owed. (The decedent and the estate are separate taxable entities.) The amount owed is based on the value of the taxable estate. In 2021, any value above the exemption amount of $11.7 million is taxed at a rate of 40 percent. 2

The value of the gross estate is computed by adding all the decedent’s assets and property, the decedent’s share of jointly owned assets, gifts and gift taxes paid within three years of death, and (in certain cases) life insurance proceeds. The value of the estate’s assets is usually determined as the fair-market value on the owner’s date of death, although other provisions apply to assets used in a farm or a closely held business (which typically has very few shareholders). 3 The value of the taxable estate is determined by deducting from that total amount any transfers to the surviving spouse, contributions to charitable organizations, debts, funeral costs, state estate tax liability, and other costs associated with administering the estate.

Married decedents can transfer any unused exemption amount to their surviving spouse, which effectively doubles the exemption for married couples to $23.4 million. 4 To account for inflation, the exemption amount is indexed to changes in the chained consumer price index (CPI).

An estate tax return is due within nine months of the owner’s death. Estates can apply for an automatic six-month extension, though, so estate tax returns for deaths in a particular year may be filed in that year or in one of the two following calendar years. Payment of estate tax liability is generally due nine months after the owner’s death. Under certain conditions, however, executors can apply for an extension. For example, estates of farms and closely held businesses can defer their tax liability and pay the amount due over 10 years.

The gift tax applies to transfers of property when the full value is not received in return. 5 Gifts below the annual exclusion amount—$15,000 per recipient from each donor in 2021, or $30,000 per recipient from married couples—are not taxable. 6 Donors who make gifts that exceed that amount are required to file a gift tax return and pay any resulting gift tax liability by April 15 of the following year.

By law, the gift tax has the same tax rate structure and exemption amount as the estate tax. 7 A donor may give as many gifts as he or she chooses to each year; the donor pays taxes on those gifts only when the cumulative amount of annual gifts (above the annual per-recipient exclusion amount) during his or her lifetime exceeds the lifetime estate and gift exemption. For example, if a donor gives a recipient a gift with a value exceeding $15,000, the donor’s lifetime estate and gift exemption is reduced by the gift’s value in excess of $15,000.

The 2017 tax act (Public Law 115-97) doubled the exemption amount for the estate tax through the end of 2025. CBO projects that the exemption amount will drop to $6.4 million in 2026 under current law. 8 People who make gifts before 2026, and estates that transfer the unused exemption to the surviving spouse before 2026, will be able to keep the tax benefit of the higher exemption amount.

Relatively few people pay estate and gift taxes. Among the 2.7 million decedents in 2016, about 13,000 estates were required to file a return—and of those, 5,500 estates owed taxes. CBO projects that the number of taxable estates will drop to 2,800 among 2021 decedents because of the higher exemption allowed by the 2017 tax act. In terms of gift taxes, about 236,000 gift tax returns were filed in 2018, but only 2,000 of those owed the tax. People who do not pay estate taxes may still be affected by them; that group includes heirs and people who engage in estate planning (the process of managing and allocating assets while a person is still alive) to avoid or lessen the tax.

Widowed decedents and people age 80 or older accounted for the majority of taxable returns filed and estate taxes paid among decedents in 2016. 9 Most estates that filed an estate tax return in that year belonged to widowed decedents who were 80 or older.

In addition, most taxable returns were filed by relatively small estates, even though most estate tax revenues came from the largest estates.

In 2018, 22 percent of taxable gifts were at least $1 million, and they accounted for 86 percent of gift tax revenues. Typically, filers must apply their estate tax exemption to the gift tax, which reduces their gift tax liability. The estate tax exemption available when those filers die, however, will be reduced by the amounts previously applied to the gift tax while they were alive.

The estate tax affects people who do not pay it directly, such as heirs. Some people engage in estate planning to avoid paying the tax (or to reduce the amount that they owe), which may result in ownership arrangements for their assets that they would otherwise not choose. For example, people might transfer assets through a trust to their heirs earlier than they had intended so as to remove those assets from their estate. 10 Although the decedent’s estate is responsible for paying estate taxes, the tax reduces the amount that heirs may receive. 11

Heirs tend to have relatively high income. Families that received an inheritance in 2019—about 3 percent of all families according to the 2019 Survey of Consumer Finances—typically had a higher median income than other families ($92,000 compared with $58,000). 12 About half of the heirs were between the ages of 55 and 75, and most received inheritances from their parents. Those inheritances did not necessarily come from a taxable estate. The median inheritance was $50,000, and the average inheritance was $186,000 (because of a relatively small number of large inheritances).

Because the estate tax is imposed on the transfer of assets, it in effect taxes people’s savings. The amount of estate tax that people pay varies—even among people with similar resources—depending on what they choose to do with their money. For instance, the tax on an estate left by someone who saves more will be higher than the tax on an estate left by someone who spends more. As a result, the estate tax could encourage people to save and invest less by making it more expensive for them to leave money to their heirs. Overall, however, the empirical evidence on the effect of the estate tax on saving is inconclusive. 13

The lack of consensus about the overall effect of the estate tax on saving stems from several factors. The smaller inheritances left to heirs because of the estate tax might induce people, or their heirs, to save more. Alternatively, estate taxes would have little effect on the saving behavior of people who do not intend to leave an inheritance. Another consideration is the way capital gains taxes apply to the value of inherited assets (see Box 1). Because of the step up in basis—upon inheritance, the cost basis of an asset is increased to its fair-market value—any appreciation in value while the decedent held the asset is not subject to capital gains taxes, which could motivate people to save more.

People who sell assets are generally subject to tax on any resulting capital gains. Those gains are typically calculated as the asset’s sale price minus its adjusted basis, or the cost of acquiring the asset. In 2021, capital gains on assets held for more than one year are subject to a maximum individual income tax of 20 percent, plus a 3.8 percent net investment income tax for taxpayers with higher income.

Assets that are held until an owner’s death avoid those taxes because their basis is “stepped up” to the fair-market value at the time of the owner’s death. When an heir sells an inherited asset, the heir’s capital gains taxes are based only on the change in the asset’s value from the stepped-up basis. 1 (For gifted assets, the recipient’s basis for the asset is the same as the donor’s—also called carryover basis.) Stepped-up basis creates an incentive for owners to hold on to their assets instead of shifting them into other uses. That lock-in effect could reduce productivity if those assets could have instead been shifted into more productive uses. Owners who hold on to their assets may incur the estate tax even if they avoid capital gains taxes, however, because those assets are included in the decedent’s gross estate. 2

Researchers have estimated that unrealized capital gains account for 34 percent to 44 percent of the value of all taxable estates, though the estimates vary by asset type and estate size. 3 Unrealized gains account for most of the value of closely held stocks and intangible assets. 4 In addition, unrealized gains as a share of taxable estates are highest among the largest estates (defined here as those with assets of $20 million or more).

Lawmakers have proposed changing the tax treatment of assets transferred at death. Among those proposals are ones that would replace stepped-up basis with carryover basis or treat transfers at death as a sale so that appreciated assets would be subject to capital gains taxes. 5 Those proposals would reduce the lock-in effect for decedents but could still affect when assets were sold. If carryover basis was adopted for inherited assets, heirs could be more reluctant to sell appreciated assets than they are now. Also, if accrued capital gains were taxed at death, then estates might need to liquidate assets to pay the tax liability due. In addition, those proposals would act as a wealth tax, so their implementation could increase the progressivity of the tax system and reduce wealth inequality. 6 To administer the proposals, policymakers would need to consider what basis to use to value a decedent’s assets if the original basis could not be determined.

1. The estate tax was repealed for people who died in 2010. Assets transferred at death in that year were valued using a modified carryover basis, but estates could instead choose to pay the estate tax under the law in effect in 2011 and thus use stepped-up basis.

2. There is evidence that the estate tax encourages people to realize capital gains. For more discussion, see Athiphat Muthitacharoen, The Impact of the Estate Tax on Capital Gains Realizations: Evidence From the Taxpayer Relief Act of 1997, Working Paper 2010-08 (Congressional Budget Office, November 2010), www.cbo.gov/publication/21941 .

3. See Robert Gordon, David Joulfaian, and James Poterba, “Revenue and Incentive Effects of Basis Step-Up at Death: Lessons From the 2010 ‘Voluntary’ Estate Tax Regime,” American Economic Review: Papers & Proceedings 2016, vol. 106, no. 5 (May 2016), pp. 662–667, http://dx.doi.org/10.1257/aer.p20161037 ; Robert B. Avery, Daniel J. Grodzicki, and Kevin B. Moore, “Death and Taxes: An Evaluation of the Impact of Prospective Policies for Taxing Wealth at the Time of Death,” National Tax Journal, vol. 68, no. 3 (September 2015), pp. 601–632, http://dx.doi.org/10.17310/ntj.2015.3.05 ; and Department of the Treasury, Office of Tax Analysis, Tax Expenditure for Exclusion of Capital Gains at Death (August 2014), https://go.usa.gov/xHW4f (PDF, 1.4 MB).

4. Closely held stocks are stocks of a company that are held predominantly by a small number of people and therefore not actively traded. Intangible assets are assets such as licenses, patents, or registered trademarks.

5. See Congressional Budget Office, “Change the Tax Treatment of Capital Gains From Sales of Inherited Assets,” in Options for Reducing the Deficit: 2019 to 2028 (December 2018), pp. 219–220, www.cbo.gov/publication/54667 ; and Harry L. Gutman, “Taxing Gains at Death,” Tax Notes Federal (January 11, 2021), https://tinyurl.com/a2tp6vrn .

6. See Natasha Sarin, Lawrence H. Summers, and Joe Kupferberg, “Tax Reform for Progressivity: A Pragmatic Approach,” in Emily Moss, Ryan Nunn, and Jay Shambaugh, eds., Tackling the Tax Code: Efficient and Equitable Ways to Raise Revenue (Brookings Institution, 2020), pp. 317–352.

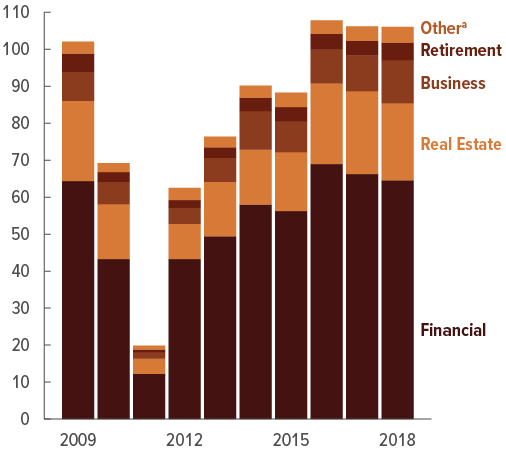

Assets of taxable estates can be classified in one of five categories: financial, real estate, business, retirement, and other (which includes works of art and depletable and intangible assets). 14 As reported on estate tax returns, those asset groupings are similar to the ones used in CBO’s estate tax model. Understanding their distribution helps CBO project estate and gift tax receipts more precisely and accurately.

In 2018, taxable estates reported $106 billion in gross assets. 15 Financial assets, which include stocks, bonds, and cash, made up the majority of those gross assets, totaling $64.6 billion. 16 The next-largest category was real estate assets, which totaled $20.9 billion in 2018. The remaining asset types—business, retirement, and other—contributed smaller amounts: $11.7 billion, $4.7 billion, and $4.2 billion, respectively.

Except in 2011, the overall composition of assets was relatively stable between 2009 and 2018 (see Figure 1). 17 Financial assets declined slightly over the period as a share of the total, from 63 percent of all assets in 2009 to 61 percent in 2018, although the dollar amount of those assets remained constant at about $64 billion in both years. As a percentage of total assets, the shares of business assets and other assets grew: Business assets increased from 8 percent of all assets in 2009 to 11 percent in 2018, and other assets rose from 3 percent of all assets in 2009 to 4 percent in 2018. In contrast, allocations of real estate and retirement assets decreased: Real estate assets declined from 21 percent of all assets in 2009 to 20 percent in 2018, and retirement assets fell from 5 percent to 4 percent over that period. 18

Billions of Dollars

Data source: Internal Revenue Service’s Statistics of Income. See www.cbo.gov/publication/57129#data .

Amounts are in nominal dollars.

Most returns are filed in the year following the owner’s death; however, because of filing extensions, some returns are filed for deaths that occurred two years earlier.

a. “Other” includes works of art, depletable assets (such as oil and gas holdings), and intangible assets (such as intellectual property products).

In 2018, the largest taxable estates—those with gross assets of $50 million or more—held 42 percent of the gross assets among all taxable estates, despite accounting for 6 percent of those estates (see Table 1). The largest estates held 43 percent (or $27.9 billion) of reported financial assets, 56 percent (or $6.6 billion) of business assets, and 67 percent (or $2.8 billion) of the assets categorized as other. The largest estates also held the greatest proportion of real estate assets (32 percent, or $6.6 billion). The rest of those assets were distributed relatively evenly among smaller taxable estates.

Data source: Internal Revenue Service’s Statistics of Income. See www.cbo.gov/publication/57129#data .

Most returns filed in 2018 were for deaths that occurred in 2017, when the filing threshold was $5.49 million in gross estate assets. Because of filing extensions, however, some returns were filed in 2018 for deaths that occurred before, when filing thresholds were lower.

a. “Other” includes works of art, depletable assets (such as oil and gas holdings), and intangible assets (such as intellectual property products).

Retirement assets followed a different pattern in 2018. The smallest taxable estates, those with gross assets of less than $10 million, held the largest proportion of retirement assets, accounting for 38 percent of the $4.7 billion in reported retirement assets. Estates with gross assets of $10 million to less than $20 million held 25 percent (or $1.2 billion) of retirement assets, and the remaining retirement assets were held by taxable estates with $20 million or more in gross assets.

Estate and gift tax revenues in 2020 totaled $17.6 billion, which was 0.5 percent of total receipts and 0.1 percent of GDP. Since 1980, combined estate and gift tax revenues have varied from close to zero as a share of GDP (or $7 billion) in 2011 to 0.3 percent of GDP (or $28 billion) in 1999.

As part of its baseline budget projections, CBO pro-jects estate and gift receipts for each fiscal year in its 10-year budget period. CBO projects that, under current law, estate and gift tax revenues would total $21.6 billion in 2021 and rise to $49.5 billion in 2031. Estate tax revenues are projected to increase sharply after 2025, when the exemption amount is scheduled to drop (see Figure 2). 19 Over the 2021–2031 period, combined estate and gift tax revenues are projected to total $372 billion. In CBO’s projections, estate and gift receipts equal less than 0.2 percent of GDP in each year of that period.

Billions of Dollars

Data source: Congressional Budget Office, using the agency’s February 2021 baseline. See www.cbo.gov/publication/57129#data .

Amounts are in nominal dollars.

To project estate and gift tax revenues, CBO uses a model that estimates the tax liability for a representative sample of U.S. households. The model projects the distribution of wealth across the population over the 10-year period, reflecting changes in the economy and demographic shifts, including changes in mortality.

CBO uses two sources of data to estimate a complete distribution of household wealth. The first source is estate tax returns, which provide information about household wealth for decedents whose wealth is greater than the exemption amount. The second source is the Survey of Consumer Finances, which provides information about other decedents. 20 Both sources are necessary to create a comprehensive measure of wealth for all decedents in a given year—those that are required to file an estate tax return as well as those with estates whose gross value falls below the filing threshold.

The model uses a sample of estate tax returns to estimate the wealth of people who died in a particular year, also known as the decedent sample. Because estates have an extended period to file a return, several years of tax data are combined to capture data representing the wealth of all people who died in a year. The model then estimates the wealth of the entire living population using the estate multiplier method, which divides the sample weights designed to approximate the population of estate tax filers by each person’s probability of death. 21

Once CBO has estimated a distribution of wealth, the agency groups assets and liabilities into categories, including stocks, real estate, business, bonds, mutual funds, cash, life insurance, and retirement accounts. The growth of each asset group is adjusted to match the most recent balance sheet data from the Federal Reserve’s “Financial Accounts of the United States.” Household wealth based on those groupings is then projected—consistent with CBO’s macroeconomic, financial, and demographic projections—over the 10-year period.

In each year of the projection period, estate tax liability is estimated on the basis of estate tax law, projected wealth, and mortality probabilities. Deductions from the value of a decedent’s gross estate are imputed using reported deductions as a share of wealth calculated from estate tax returns. For each estate, the model estimates its potential tax liability and assigns it a mortality risk based on the age and sex of the owner. (For married couples, the mortality risk of the estate is the probability that both spouses will die in the same year.) Mortality risks are adjusted to reflect differential mortality for individuals who purchase annuities from life insurance companies. 22

For gift taxes, CBO projects revenues on the basis of projected wealth , economic conditions, and historical relationships between those variables and actual revenue collections. In addition, gift tax receipts are adjusted for anticipated changes in the exemption amount and tax rates.

CBO’s projections of estate and gift tax revenues are meant to reflect the middle of the distribution of possible outcomes. Actual year-to-year changes in receipts may be more volatile, reflecting the inherent uncertainty about people’s motivations and behavior. In the past three years, for example, revenues projected early in the previous year were higher than actual revenues by 1 percent (2020), 15 percent (2019), and 3 percent (2018). 23 Particular sources of uncertainty include the following:

1. A related provision, the generation-skipping transfer tax, applies to certain transfers made directly to a recipient more than one generation younger than the donor. That provision is intended to limit the amount of estate and gift taxes that can be avoided. It is not examined in this report.

2. In 2021, the estate tax rate begins at 18 percent on the first $10,000 in taxable transfers and reaches 40 percent on taxable transfers over $1 million. (Taxable transfers comprise taxable gifts and transfers at death.) Because a credit effectively exempts $11.7 million in taxable transfers, the tax rates below 40 percent are not applicable.

3. Executors can choose an alternate valuation date that is six months after the owner’s death (or the date on which assets are sold or otherwise transferred if that occurs within six months of the death) if it would result in a lower valuation of the estate. In addition, executors can value assets used in a farm or a closely held business at their value as they are currently used (or productive value) rather than their fair-market value, or they can discount the value of those assets owing to the heirs’ lack of control as minority owners and the assets’ lack of marketability.

4. If a married decedent leaves his or her property to the surviving spouse using the spousal deduction, the decedent’s estate is not subject to the estate tax; however, once the surviving spouse dies, the estate potentially becomes subject to the estate tax if its value exceeds the exemption amount.

5. In the tax code, gifts are distinguished from donations, which are given for charitable purposes and may be deductible from income taxes.

6. Other nontaxable gifts include transfers to charitable organizations, transfers to spouses, and payments made directly to educational institutions or medical providers on someone’s behalf. Exclusion amounts for the gift tax are indexed to changes in the chained CPI.

7. In practice, the gift tax is lower than the estate tax. That is because the gift tax is calculated on the basis of the amount received, whereas the estate tax is calculated on the basis of the value of the entire estate, including the assets used to pay the estate tax.

8. Current law provides for a $5 million exemption with an adjustment for inflation. According to CBO’s projections of the chained CPI, the exemption will be $6.4 million in 2026.

9. See Internal Revenue Service, Statistics of Income Tax Statistics, “Estate Tax Data Tables, Selected Years of Death” (accessed January 8, 2021), https://go.usa.gov/xHjC2 .

10. A trust is a legal arrangement in which assets are held or used by a person or entity for the benefit of another person. There are many types of trusts, and they are generally governed by state laws. One such type is an irrevocable trust, which is commonly used because it places assets outside of the grantor’s estate and therefore not subject to the estate tax; however, once the trust is established, the grantor loses control of the assets and cannot change the terms of the trust.

11. An alternative to the estate tax is an inheritance tax under which heirs are responsible for paying taxes on the assets transferred to them. For more discussion, see Joint Committee on Taxation, Description and Analysis of Alternative Wealth Transfer Tax Systems, JCX-22-08 (March 10, 2008), www.jct.gov/publications/2008/jcx-22-08 (PDF, 102 KB).

12. Median family income is the income dividing families into two equal groups. For example, half of all families that received an inheritance had an income that was below $92,000, while half had income above it.

13. For a recent summary of the behavioral effects of estate and gift taxes, see David Joulfaian, “What Do We Know About the Behavioral Effects of the Estate Tax?” Boston College Law Review , vol. 57, no. 3 (May 2016), pp. 843–858, https://tinyurl.com/2bnnbafd . For more discussion of the behavioral effects of estate taxes on people’s work, saving, and charitable contributions, see Congressional Budget Office, Federal Estate and Gift Taxes (December 2009), www.cbo.gov/publication/41851 ; and Joint Committee on Taxation, History, Present Law, and Analysis of the Federal Wealth Transfer Tax System , JCX-52-15 (March 2015), www.jct.gov/publications/2015/jcx-52-15 (PDF, 263 KB).

14. Depletable assets are those whose use is subject to exhaustion, such as oil and gas wells or other natural deposits. Intangible assets include licenses, patents, and registered trademarks.

15. Most returns filed in 2018 were for deaths that occurred in 2017, when the filing threshold was $5.49 million in gross assets. Because of filing extensions, however, some returns were filed in 2018 for deaths that occurred before 2017, when filing thresholds were lower. A small number of estate tax returns were filed for deaths that occurred in 2016.

16. Assets were placed into one of five categories based on the type of property that was reported on the estate tax return.

17. The filing threshold rose from $2 million for people who died in 2008 to $5.49 million for people who died in 2017. In 2011, the amount of assets reported was unusually low, owing to the repeal of the estate tax for people who died in 2010. (Estates had the option of paying the estate tax in effect in 2011 instead.)

18. Retirement assets include annuities, assets held in defined contribution plans (such as individual retirement accounts), and the taxable portion of survivors’ benefits from defined benefit plans (such as employer-provided pensions).

19. For revenue projections by category, see the supplemental data published with Congressional Budget Office, The Budget and Economic Outlook: 2021 to 2031 (February 2021), www.cbo.gov/publication/56970 .

20. The exemption amount has risen over time. In 2018, the most recent year for which tax data are available, the exemption was $11.18 million. CBO also used data from earlier years to create the distribution—for example, estate tax returns from 2001 decedents were used to fill in the sample between $1 million and $5 million.

21. For more discussion of the estate multiplier method, see Aaron Barnes, Personal Wealth, 2013, Statistics of Income Bulletin (Internal Revenue Service, Winter 2019), https://go.usa.gov/xHD9A (PDF, 563 KB).

22. Those calculations are based on estimates from Olivia S. Mitchell and others, “New Evidence on the Money’s Worth of Individual Annuities,” American Economic Review, vol. 89, no. 5 (December 1999), pp. 1299–1318, https://tinyurl.com/2addujyd . For information about wealth’s effect on death, also see Jeffrey R. Brown, “Differential Mortality and the Value of Individual Account Retirement Annuities,” in Martin Feldstein and Jeffrey B. Liebman, eds., The Distributional Aspects of Social Security and Social Security Reform (University of Chicago Press, January 2002), www.nber.org/chapters/c9756 .

23. See Congressional Budget Office, The Accuracy of CBO’s Budget Projections for Fiscal Year 2020 (December 2020), www.cbo.gov/publication/56885 , The Accuracy of CBO’s Baseline Estimates for Fiscal Year 2019 (December 2019), www.cbo.gov/publication/55927 , and The Accuracy of CBO’s Baseline Estimates for Fiscal Year 2018 (December 2018), www.cbo.gov/publication/54872 .

24. Researchers have found that gift giving between a parent and child while the parent is still alive can depend on the parent’s lifetime income and the child’s income; gifts to a child increase as a parent’s income rises but decrease as the child’s income rises. See, for example, Joseph G. Altonji, Fumio Hayashi, and Laurence J. Kotlikoff, “Parental Altruism and Inter Vivos Transfers: Theory and Evidence,” Journal of Political Economy, vol. 105, no. 6 (December 1997), pp. 1121–1166, https://doi.org/10.1086/516388 .

This report, which is part of the Congressional Budget Office’s continuing effort to make its work transparent, explains how CBO prepares revenue projections for estate and gift taxes. In keeping with CBO’s mandate to provide objective, impartial analysis, the report makes no recommendations.

Shannon Mok and James Williamson prepared the report, with guidance from John McClelland and Joseph Rosenberg. Tess Prendergast assisted with data collection and analysis. Ann Futrell, Nadia Karamcheva, Jeffrey Schafer, Jennifer Shand, and Ellen Steele provided helpful comments on the draft. Madeleine Fox fact-checked the report.

Mark Doms and Robert Sunshine reviewed the report. Christine Bogusz was the editor, and R. L. Rebach was the graphics editor. This report is available on CBO’s website ( www.cbo.gov/publication/57129 ).

CBO continually seeks feedback to make its work as useful as possible. Please send any comments to communications@cbo.gov .